In a few words, Payday lending is defined as a type of short-term borrowing where an individual borrows a small amount at a very high rate of interest Payday Loan Definition | Investopedia. In the 90’s, these services were offered via Payday loan stores. In today’s economy, storefront small loan-dollar market (i.e. Insta cheques) has shifted, like many others, into the web. According to preoccupying results of the Pew Charitable Trusts’ study, dated October 2014, Internet payday lenders are currently doing business under deficient controls and regulations Fraud and Abuse Online: Harmful Practices in Internet Payday Lending.

In a nutshell, this American report outlines the following facts:

Aggressive Pricing Lump-sum loans online typically cost $25 per $100 borrowed per pay period, an approximately 650% annual percentage rate. For an average payday loan of $375, borrowers pay a $95 fee online compared with $55 through stores.

Bank account vulnerability Before borrowers typically had to provide a post-dated check in the amount they wished to borrow plus a fee. Nowadays online lenders depend on banks to facilitate their loans via Electronic Fund Transfer. Online lending places consumer bank accounts at risk. Borrowers report overdrafts, unauthorized transactions, and the loss of accounts as a result of online lending practices. (p. 13)

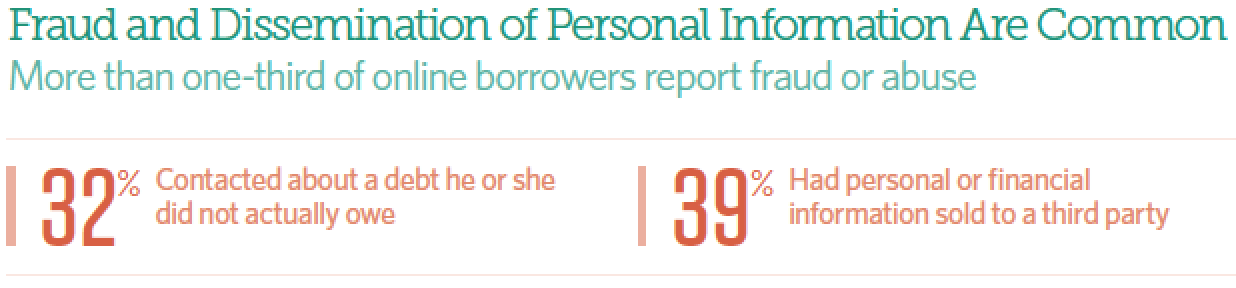

Customer acquisition Most lenders rely at least in part on lead generators: companies that collect information from potential borrowers searching for loans and then sell it to lenders (p.5). Lenders paid in 2011 as much as 125$ to acquire borrower’s personal information.

Lack of transparency Lead generators do not disclose the lenders’ identity. Hence, borrowers usually lean their prospective lenders’ name only after they have provided their personal and financial information or even after they have received funds.

Dissemination of personal information After a lender buys a lead, the borrower’s information remains available for sale. This practice of reselling leads creates opportunities for fake debt collectors and others to buy the information and attempt to collect money using aggressive tactics. Richard Cordray, director of the Consumer Financial Protection Bureau says:

« The highest bidder may be a legitimate lender, but it could also be a fraudster that has enough of the consumer’s sensitive financial information to make unauthorized withdrawals from their bank account. » (p. 11)

Canadian Market Regulation

Pew’s report does not include per se a Canadian market study but a quick keyword search makes me presume that this industry has no real territorial boundaries. So… Can we therefore feel safer here on our side of the fence?

Quebec Civil Code and Consumer Protection Act In Quebec, consumer rights are protected based on the general principal of good faith. Me Nathalie CROTEAU – Université de Sherbrooke has made in « Le contrôle des clauses abusives dans le contrat d’adhésion et la notion de bonne foi (1996) » the following statement:

La valorisation de la notion de bonne foi a un effet marqué sur le regard que les tribunaux portent sur les relations contractuelles et démontre clairement que la morale et l’équité ne sont pas absentes du droit des obligations.

When it comes to payday lending, in most cases, the borrower is a consumer. This right opens the door to lesion and the Consumer Protection Act. The Court has expressed itself in Bégin c. Marcouiller, 2007 QCCQ 7742 with the following words: « Le prêt d’argent dont le coût excède d’une manière exagérée la normalité ou qui est assorti d’un taux usuraire est, en principe, lésionnaire » (see art. 1406 Q.C.C.). Therefore, any situation where there is a serious disproportion creates a presumption of exploitation. Consumers can also rely on article 1437 Q.C.C.’s protection regarding abusive clause in a consumer contract. The remedies are well explained in Crédit excellence ATG, s.e.n.c. c. Néron, 2011 QCCQ 221, where the court may pronounce the nullity of the contract, order the reduction of the obligations arising from the contract or revise the terms of the agreement article 2332 C.C.Q. :

« Les Tribunaux ont souvent eu à se prononcer sur le caractère abusif ou lésionnaire des taux d’intérêts réclamés par des prêteurs, soit en vertu des articles 8, 9 et 115 de la LPC, soit en vertu des dispositions de l’article 2332 du Code Civil« .

Profit driven crime In Canada, loan « sharking » is officially designated as a criminal offence if the rate exceeds 60% per annum (see definition of Criminal Interest Rate section 347(1). Hence, the federal Minister of Justice, introduced in 2007 an exemption giving all provinces the right to regulate Payday Lending in Section 347.1(2): Section 347 will not apply to a person in respect of a Payday loan, if (a) the amount is $1,500 or less and the term is 62 days or less; (b) the loan broker is licensed under the laws of a province to offer Payday loans; and (c) the province has legislative measures that protect borrowers which provide limits on the total cost of borrowing. Ontario legislation adopted the Payday Loans Act, 2008, SO 2008, c. 9 in coordination with the federal legislation. Any person is prohibited from acting as a loan broker in Ontario without a loan broker’s license licensed in accordance with under the Act. The Director v. The Cash Store, 2014 ONSC 980. I did not find anything similar with the Office de la protection du consommateur.

One last thing!

Tom Naylor, Professor of Economics at McGill, mentioned in his report to the Department of Justice Canada 2003-07-02 Table of Contents (3.4):

« It seems that loan-sharking is seen, in the eyes of law enforcement (as distinct from in the eyes of the law), not as a problem per se but only as a problem when carried on by a certain type of individual in a certain milieu (i.e., the notion that it is an important source of income to “organized crime”). In terms of the two salient characteristics of loan-sharking, the first being extremely high rates in relation to market norms is certainly true – although whether the rates are really so high in relation to risk, no one can say a priori. As to the second, the use of violence or its threat to ensure repayment, it makes the trade approximate a predatory practice like extortion. »